I’ve always been around people older than me since I started working. I was the youngest in my office so my colleagues would give me advice on various topics, about ‘‘mistakes’’ they’ve made related to anything - money, relationships, shopping, getting a loan, etc and I listened. I started gathering information, after all, it was all free, and coming from live examples too. I got my first credit card in 2017 and my brother gave me all the guidelines to stay on track as he was working for American Express then.

So, let’s bring them out. The graphics in this newsletter can be downloaded to your phone gallery and shared with your friends or colleagues who are looking to apply for a credit card. I hope you’ve read the basics though, if you haven’t, read here..

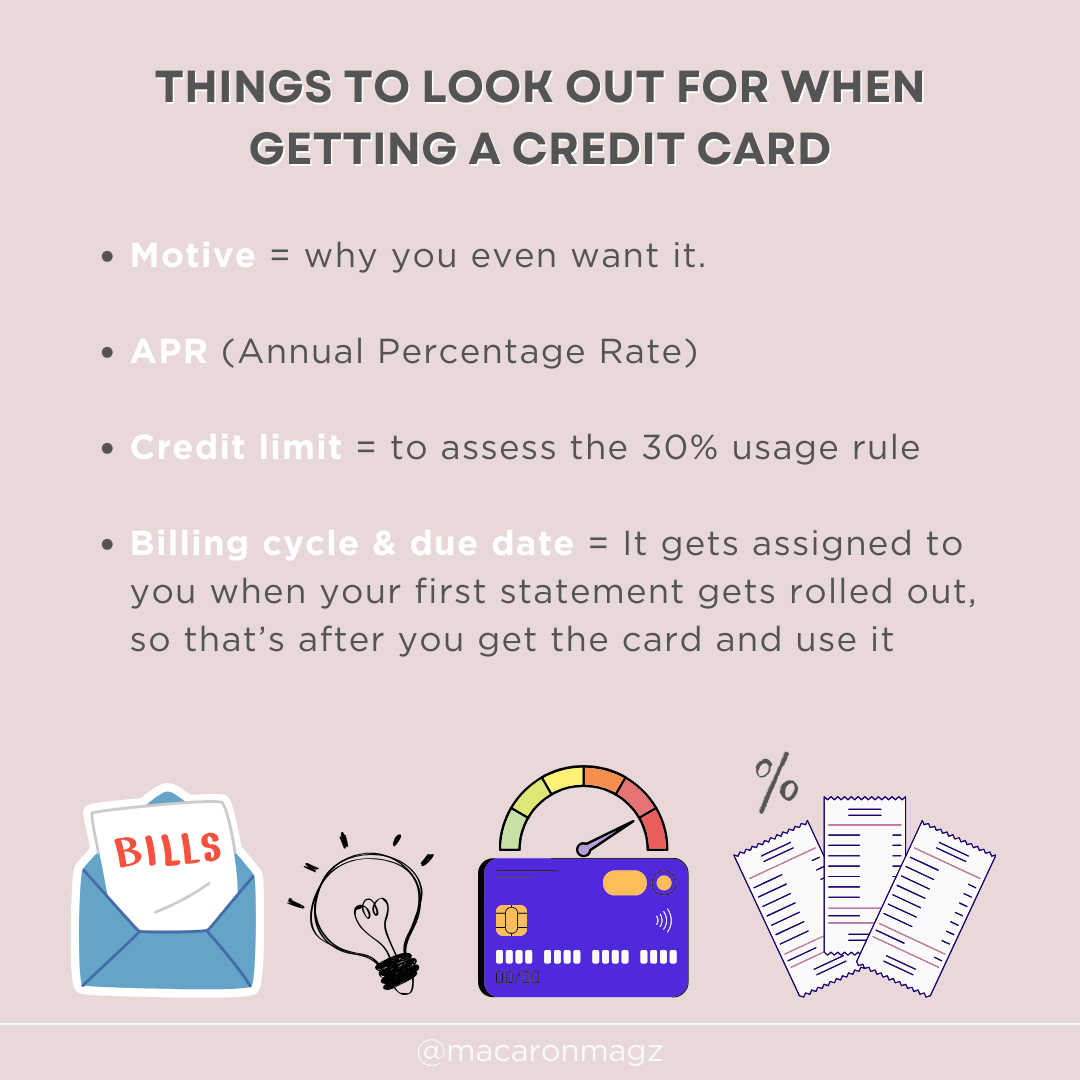

Things to quickly find out when getting a credit card:-

why you even want a credit card = motive,

APR (annual percentage rate),

credit limit = to assess the 30% usage rule,

Billing cycle & due date = It gets assigned to you when your first statement gets rolled out, so that’s after you get the card and use it.

If you want a credit card because people around you have it, please don’t let that be a reason to get it. When you apply, they will do a credit check and check scores, which also means it will drop your scores by a few points and the inquiry will be recorded on your credit report for 2 years. And, if you don’t use the credit card for a month or two, the bank will automatically cancel your card because banks have to incur a cost for maintaining every card they issue and they do not need your permission to cancel it. So, all that effort over FOMO- wasted.

What if I use the entire card and pay the bill in full every month? I am paying it in full so it shouldn’t be a problem right? ……The question below has the answer…

Why only use 30% of the entire limit of the card? - To show the banks that you’re a good borrower. It comes under the ‘Credit utilization rule’ and going over or consuming your entire limit every month impacts your scores negatively. It can sometimes become difficult to stay under 30% so it’s advisable to stay under 50%. (Read the important tip at the end)

APR is the amount of annual interest rate the bank will charge you on your credit card on missed payments. I went to one of the credit card provider’s websites to show you what I am talking about. By the way, all this info about the card you want is readily available on your bank’s website so you can easily shop around.

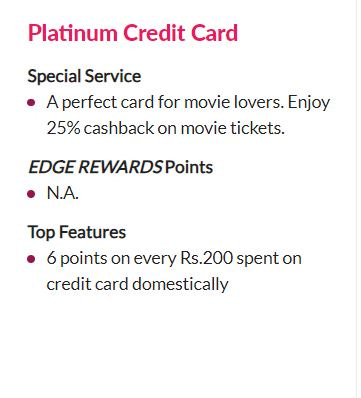

They provide you with a list of cards they offer with different benefits, some could look like this -

And, when you click on the details of the card, you see all the charges pertaining to the card, the list was quite long so I took a screenshot of some parts -

(My apologies for the smaller print, I am still learning my way around many tools.)

Just to draw a comparison, interest on credit cards is almost always higher than taking a personal loan (approx. 11% - 15%) or a car loan (approx. 8% - 10%). So, find out your billing cycle & due date quickly (always mentioned on your statement right from the start) so you can avoid these interest charges, how? - by paying the bill in full (even if the statement says you can make a minimum payment)

!! Alert !! Boring example calculation ahead …. but very important !!!

Example - My credit card bill is Rs 15,000 and the statement says I have an option to pay just the minimum amount of Rs 2,000 and the rest can be paid off later or next month. So, if I pay only Rs 2,000 now, next month I’ll have a balance of Rs 13,000 plus whatever the next purchases I make.

I will be paying interest for sure because I did not make a full payment. I also need to understand that I will NOT be paying interest on Rs 13,000 but on the full Rs 15,000. Whatever currency you’re dealing with, this calculation applies.

Important tip - For times you can’t make a full payment, pay the minimum and do not miss it. Banks report your payments every month to the credit bureau, that’s how your credit report gets updates and scores change from bad to good, to good to better.. Even when not paid in full, that payment gets recorded in your favour and it keeps your score stable. Your score only gets negatively impacted when you’re not paying full over and over again. Once or twice does not drop your score, they just don’t grow.

But remember, missing the payment drops your score immediately.

Paying the minimum amount has a quick way of becoming a vicious circle garnering a lot of interest and debt. Avoiding it is always the best. That being said, our life is very long with us going through many stages in our life financially. I know I have been there, and so many around us. Keep the minimum pay option for absolute emergencies because emergencies do occur. They’re inevitable. And, don’t judge yourself so harshly for doing it. It happens. As long as you’re working towards your goals, all is well.